On March 21, 2022, the U.S. Securities and Exchange Commission (SEC) released a comprehensive set of proposed rules mandating climate-related risk disclosures for public companies. The Proposed Rule requires a public company to make more robust disclosures in its periodic reports with the SEC regarding its exposure to climate-related risks and its impact on the environment, focusing primarily on emission of greenhouse gases. The Proposed Rule draws significantly from the guidance provided by the Task Force on Climate-Related Financial Disclosures (TCFD) and the Greenhouse Gas Protocol.

Timing

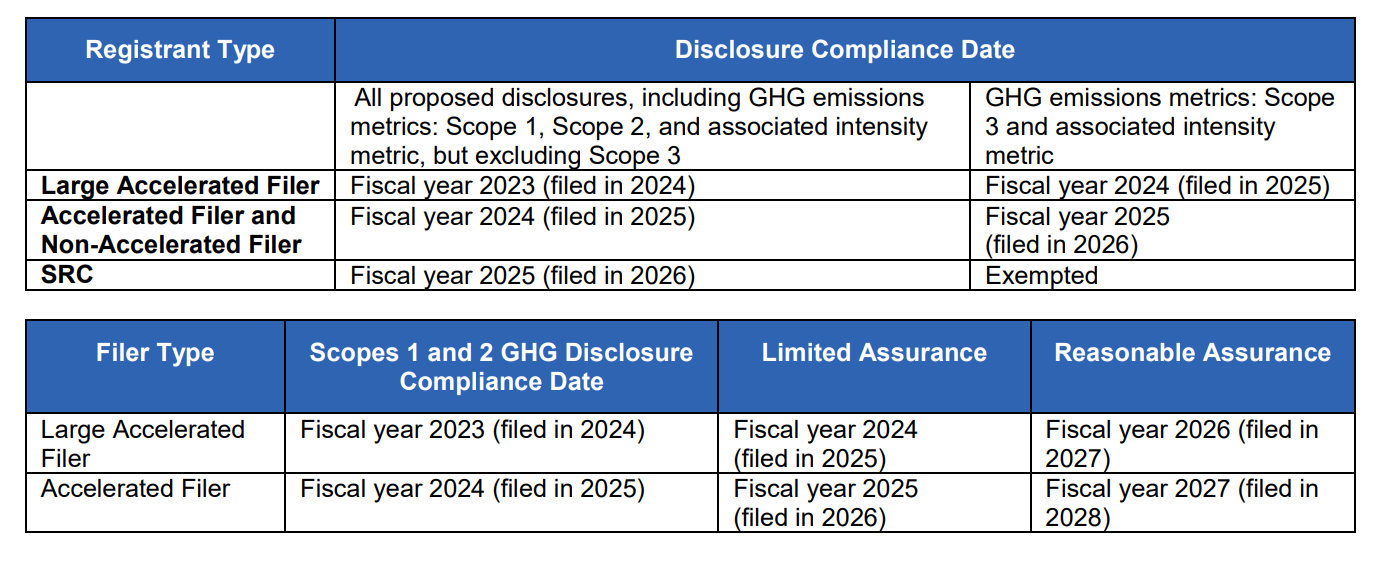

The proposed ruling was released on March 21 and is available for public comment for 60 days through the SEC website. The SEC currently anticipates finalizing the proposed rule in December 2022. If this timing is met, the earliest filers would be required to disclose climate-related information in 2024, covering their FY2023 activities.

Source: SEC

Source: SEC

It is important to understand that the proposed rule could change substantially before finalization. While we recommend that clients assess their potential gaps in existing disclosures versus the proposed rule, it may be premature to revise your 2022 or 2023 reporting strategy.